How well do you know how a bicycle works? Many of you, myself included would have said “very well.” I learned to ride a bicycle as a toddler and, although I don’t ride frequently now, I’m very familiar with bicycles. Or I thought I was. I recently read an article that asked the following questions about bicycles to other people who reported to be familiar:

Could you draw one? Artistic skill aside, could you identify a picture of a functional bicycle against non-working photos?

40% of people in the survey made a fundamental mistake in drawing how a bicycle’s chain functions. This survey built on a 2002 study that found people rate themselves as having a far greater level of understanding of complex phenomena before being asked to describe its mechanics than they report after having to give a description. The study coined the phrase the illusion of explanatory depth.

The illusion of explanatory depth is phenomenon where individuals believe they understand the world with far greater detail than they actually do. The illusion of explanatory depth is not a function of blind overconfidence, or a person’s inability to admit ignorance; rather it is a function of a miscalibration of a person’s ability to understand and explain complex systems with detail. Because I interact with my refrigerator daily, and am familiar with what it does, I am pretty sure I know how it works. Or I have a pretty good idea, until I have to diagram or explain how it works.

Self-testing one’s knowledge of explanations is difficult. Testing knowledge of facts is easy. I either know that coriander and cilantro are the same plant or I don’t; it is much harder for me to challenge myself on what exactly coriander brings to a dish and how it changes the flavor of my food. Even when I am able to test myself, it’s harder for me to hold myself accountable; systems are harder to Google.

I recently had the opportunity to test my understanding of complex systems that I felt insatiately familiar with–my own cooking. I knew that I add oregano to my sauce when I make spaghetti, and cumin to a Middle Eastern inspired chicken dish. When I add these spices, am I adding them because I am looking to bolster or change a certain quality of the food, or because I know that the spices “belong” with the dish.

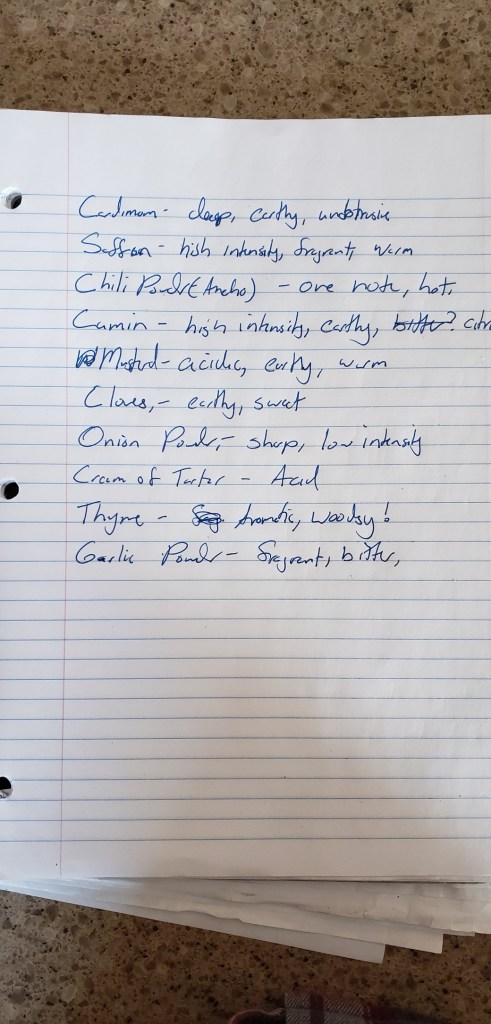

To test my knowledge of the spices in my kitchen I wrote down my impressions of each spice in my spice drawer:

Yeah, I know I should have more whole spices.

I described no fewer than three spices as “warm and earthy.” How would one describe cinnamon? How does that description differ from turmeric? Allspice? How about garlic? Onion? I was amazed at how poorly I described spices that I used daily:

My handwriting could use some improvements as well.

After a confidence-crushing attempt, I wanted to compare my pre-tasting notes with my experience tasting each spice individually. I set up a spice tasting:

First, I poured about a 1/4 teaspoon of a spice on to a plate and smelled it. I recorded my impressions on an index card.

Second, I tasted the spice from the plate and wrote my impressions on the same index card.

Third, I toasted the spice in a pan and noted how both the smell and flavor changed after toasting.

Between each taste, I took a bite of an apple to cleanse my palate. Between each smell, I smelled a ramakin filled with coffee grounds.

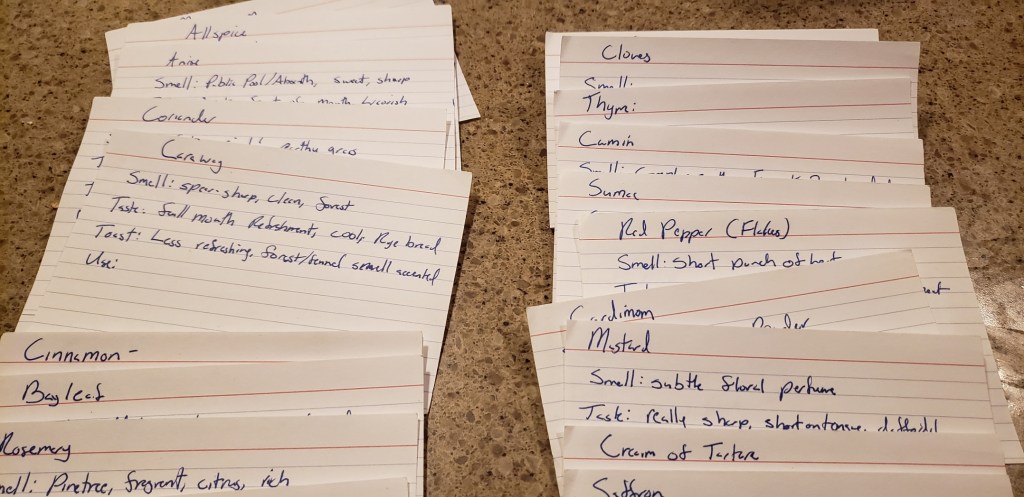

I ended with a series of notecards (pictured below) that captured a much more accurate and personal description of the spice. During the tasting, I found that I was able to describe, with much more precision, flavors and smells that I was confident I knew prior.

My handwriting did not improve that afternoon.

Exploring my spice jar with intention was humbling and promises to be helpful in future food endeavors; but isn’t exactly profound. In his recent book, The Data Detective: Ten Easy Rules to Make Sense of Statistics, Tim Harford presents examples of how the illusion of explanatory depth heightens political polarization. Study respondents who had strong views on complex policies, such has cap-and-trade programs, were more willing to alter their views after being asked to describe the program. These study respondents realized, as I did about my own cooking, that they had miscalibrated how much they actually understood the mechanics of the programs they were previously passionate about.

Understanding how the illusion of explanatory depth impacts our worldview is helpful, but does not solve the problem that self-testing one’s knowledge of explanations is difficult. There is at least one tried-and-true method:

If you want to learn something, try teaching it.

Richard Feynman

The Feynman technique is a four step process to learning something. It can be applied to physical skills, fleshing out ideas, or confirming your reading of the daily news. The steps are as follows:

Identify the subject

Explain it to a child (or an imaginary child)

When part of your description is missing detail or a link between information, study the gaps in your knowledge

Simplify, fill the knowledge gaps, and explain again

The act of explaining concepts is a natural test to determine how well we understand the components of complex phenomena. Teaching disrupts the illusion of explanatory depth, because it requires explanatory depth.

How well do you know your bicycle, food, or passionate views?

Want to learn more about the idea of illusion of explanatory depth? Find more below:

For a few days at the end of January 2021, GameStop, a brick-and-mortar video games retailer commanded every news headline. The company’s stock price, valued at $2.57 a share in April 2020, rocketed to a high of $483 a share on January 28, 2021. The company, formally valued around $300 million in market cap, was briefly worth $25 billion. There were no changes in the business that accounted for the change in price.

As of February 12, GameStop is trading at $52.40 a share. More than the paltry $3, but nowhere near its high. The GameStop rollercoaster is over.

Or is it? Although the stock price is beginning to level out, the controversy around GameStop is not yet over. After the stock price jump, and subsequent fall, market insiders and retail investors have started asking for additional regulation to protect their interests. The regulatory response battle will be a long one.

Hedge funds shorted the stock and there was opportunity to profit from a “squeeze.”

The second reason requires a little bit of explanation. John Cochrane describes the short selling process clearly in his blog:

Here’s how it works. A has GameStop shares. B, the short seller, borrows those shares from A, and sells them to C. Now both A and C can have long positions in the stock. We have doubled the supply of shares. Alas, this mechanism is imperfect. It only lasts a day. B must be ready to buy back the shares the next day and return them to A.

The shorts have two options, if the price does not fall:

Close the position– Pay the market value + interest for the stock to buy the underlying shares. Because B has to buy the stock at market value (that did not fall), B owns the shares and the price of the stock increases due to the increased demand.

Roll the position –B does not need to give the stock back on day 2, instead paying more interest each day to continue borrowing the shares from A.

The short selling of GameStop was so prolific that the shorts (B) borrowed more shares than have been issued. The WallStreetBets Reddit and YouTube communities jumped on the opportunity to buy shares, in the expectation that the shares would have to be bought at higher prices by the short selling entities. These communities have become increasingly large over the last few years, corresponding with the rise of fee-free brokers. Fee-free brokers with applications, such as Robinhood, allow individuals with any sum of money (the average account is less than $5,000 and owned by a 31-year-old) to participate in the stock market. Robinhood has over 13 million users; at the GameStop trading peak, analysts predict that nearly 50% of Robinhood users bought GameStop.

The squeeze started on January 12. On January 12, the stock closed at $19.95 per share. January 13? $31.40. January 25, $76.79. January 26:

January 27 closed at $347.51 per share. By February 2, the stock closed under $100 a share and the principle short sellers had closed their positions.

How did institutions respond?

During the period between January 26 and February 2, the stock was halted or paused a number of times by brokers and the New York Stock Exchange.

Robinhood, and similar broker-apps, restricted trading of GameStop and other highly volatile securities during this time. Users were, at times unable to purchase more shares or options of GameStop. Other application users reported that Robinhood actively sold their shares or options of the company, at low prices. Retail investors, understandably complained and demanded action from Washington:

LMAO omg I love when ppl w differences come together. Beautiful day out here on Twitter pic.twitter.com/uQ9xBany2j

These brokers were quick to respond that they were forced to halt stocks and restrict ownership based on current regulation or clearinghouse requirements.

When a Robinhood user buys a stock it actually takes two days for the funds to be exchanged (SEC standard), in the interim, Robinhood must post the colleterial for its users’ purchases. Due to Dodd Frank regulation, clearinghouses must set collateral requirements based on concentration of ownership and volatility of a stock. These brokers are not able to use their clients money to post colleterial (the theory is that these restrictions will prevent brokers from irresponsibly losing investor money when they go bust). Depending on the broker, either the clearinghouse forced a halt trading on GameStop, or the broker no longer had the liquidity required to cover the collateral requirements for trading the stock. As an example, the largest clearing organization (DTCC) reported that the industry-wide collateral requirements jumped from $26 billion to 33.5 billion on January 28.

Large institutional traders did not have the same liquidity concerns and were not halted by their clearinghouse agreements from purchasing the stock, or its derivatives.

So who made money?

The GameStop short squeeze was billed as a David-and-Goliath story of Reddit users taking down hedge funds. That isn’t exactly what happened. Short sellers initially lost around $19 billion, but none shuttered. It’s true that Melvin Capital (the hedge fund with the largest short position) required a bailout of about $3 billion from other funds, but hedge funds as a whole were not defeated by the short squeeze. Who made all of the money from the stock increase?

Not retail, generally. GameStop saw a $20.4 billion gain in market cap. Nine investors, led by Fidelity and BlackRock, totaled a $16 billion return on the GameStop short squeeze. These 9 firms made 75% of the total gain.

The returns were mixed for retail investors. Some early retail investors saw significant gains from their GameStop investment, most bought over $100 per share and received only modest gains or, more frequently, losses. When Robinhood limited its users’ ability to purchase stock or sold shares purchased with unsettled funds, retail investors were prevented from capitalizing on potential money making opportunities.

Will it happen again?

I am not a financial advisor, nor do I give financial advice. I am speculating on the frequency of a similar short scenario; rather than on the performance of any individual stock.

For a short squeeze of this magnitude, institutional players must have interests on both sides. Michael Burry and other investors publicly announced long positions in the company. Short institutional firms announced their interests as well. These types of public battles don’t occur often. Firms that take anti-shorting actions tend to have very low returns, making them unlikely targets for long-term value investors. For all of the publicity Robinhood and WallStreetBets received in the GameStop narrative, they did not have the power to push the GameStop stock alone. As noted above, the firms that cashed in on the run were major hedge funds. Institutional money was required to generate the momentum in the stock price.

Second, the short interest in GameStop was greater than the number of shares in circulation. As of February 12 2021, there are no companies in the S&P 1500 with short interest over 100%. While short squeezes occur with short interest well under 100%, the magnitude will not reach GameStop levels.

Retail short squeezes might become more common though. Small retail investors will attempt to replicate the GameStop experience on other stocks. Chat rooms, Reddit, and YouTube are not diminishing in size. The WallStreetBets Subreddit (community blog) grew by 2.4 million subscribers during the GameStop short squeeze.

Robinhood continues to grow as well. The tool enables small retail investors to trade stocks, as well as more complex derivatives, without fee. The rise in this app enabled a major rise in speculative investment by individual retail investors (the common folk).

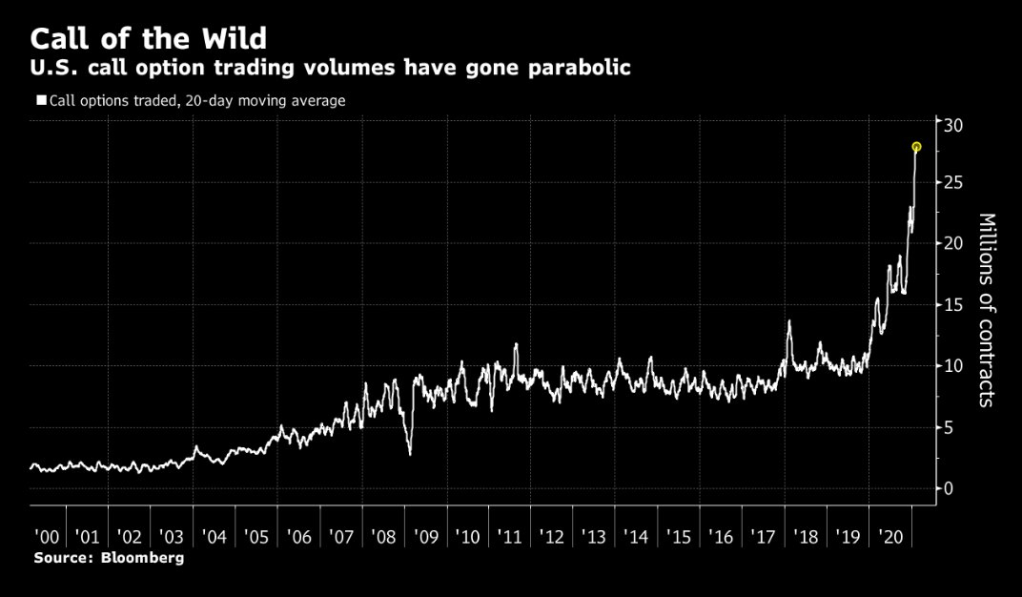

After the introduction of transaction-free brokers, such as Robinhood, the number of options traded skyrocketed.

Another GameStop is unlikely, but the increase of speculative investing by small retail accounts will fundamentally change the trading behavior of some stocks. About a year ago, WallStreetBets pushed the stock of Lumber Liquidators through community action. The Lumber Liquidators example is more representative of the market power of the WallStreeBets community. I anticipate more of those stories as the platform grows and barriers to trading are removed through applications such as Robinhood.

If it’s unlikely to happen often, why should I expect regulatory action?

Regulators are receiving pressure from institutions and retail investors to prevent similar situations from happening. On the institutional side, the demand for regulation includes a crackdown on these forums to prevent coordination on certain stock strategies. Institutions calling for greater regulation of social media coordination point to the behavior as a form of market manipulation. GameStop is not the only stock that had a semi-coordinate strategy. The WallStreetBets community tried, to a lesser extent, to exert the same pressure on AMC, Nokia, and BlackBerry.

Retail investors are arguing for regulation that would further democratize the stock market. The nature of these regulations would be to open the number of investment vehicles available for retail investors, to protect trading chat rooms (CNBC is allowed to exist, how is a Reddit forum discussing stocks fundamentally different), prevent clearinghouses from being able to raise collateral requirements in a manner that restricts retail trading.

Although the nature of the regulation that will be introduced is unclear, it’s reasonable to expect a regulatory response. Treasury Secretary Yellen scheduled meetings with the SEC, the Federal Reserve Board, the New York Fed and the Commodities Futures Trading Commission to discuss the recent events in the market. Given the Tweets above, members of Congress are interested in proposing regulation as well. The CEOs of Robinhood and Reddit will testify this month before a House Committee.

Our regulatory system does a lot in the name of “protection” to keep people of low means away from the kinds of investments that wealthy people can access. I think it is likely that the majority of the regulation that comes from the GameStop hearings will attempt to limit “risky” retail behavior, rather than open the market further. I anticipate at least some of the following regulations will be put into place:

Small-broker applications will be reclassified as gambling applications and regulated in the same manner as sportsbooks (state-level)

Small-broker applications will need to change their user interface to reduce gamification of stock trading

Create minimum equity requirements on trading accounts that are able to trade derivatives

Create a framework for the SEC to hold forums accountable for any coordination on stocks that occurs on the platform

Although the GameStop story received a lot of press, its impact on the stock market and financial institutions of the United States was marginal. Any of the likely regulations above would almost certainly do more harm than was created by the GameStop short squeeze.

*Addendum–The relationship between broker applications and organization that purchase order flow was not addressed at all in this write-up. The example commonly found in the news is a relationship between Citadel and Robinhood. I intentionally left it out because it is not unique to the GameStop scenario, nor does it related to the underlying activity; however, I see these relationships as an area fertile for proposed regulation.

Economists are constantly inventing new weighing mechanisms to evaluate the overall health of the economy. Because the US economy is a massive, ever-changing, complex system comprised of independent and semidependent actors, no single number or equation has sufficed to gauge the heath of the economy.

I will not present a grand unifying economic theory.

Economists track a number of economic indicators to determine the health of the economy. Some indicators are leading, meaning they predict changes in the greater economy. Others are trailing, meaning they measure factors of the economy that already occurred. Given the complexity and velocity of the macro-economy, it operates with a sort of Heisenberg uncertainty principle that prevents a truly current understanding of economic health.

One of the most important leading economic indicators that policy makers use is the Consumer Confidence Index (CCI). The Consumer Confidence Index tracks responses to a monthly survey sent to consumers about their perceptions for business, employment, and income for the next six-months. Currently, the model indicates that the US is at lower-than-average confidence; however, I have reason to doubt the results.

Allow me to propose one more model for consideration. The percentage of “_________ as a Service” sales compared to total sales for the following industries:

Tech (enterprise, personal, and public sector)

Food

Automotive (leases)

Consumer non-durables

“_______ as a Service” or XaaS describes a model where consumers purchase a subscription for a product, rather than the product itself. In these agreements, the consumer pays a regular payment in exchange for usage of the product and the necessary support to maintain the product. At the end of the agreement, the consumer has no right to the product and must purchase a new subscription to continue use. Automotive leases are an example of cars as a service: consumers pay a lease to use the car each month and for the dealership to handle maintenance through the lease period.

Purchasing anything as a service requires confidence in an ability to pay for the product through and after the subscription term. If I anticipate a huge pay cut in three years, I will not start a lease. Instead, I’ll purchase a less expensive vehicle (finance if needed) that I will retain after my payments are through. Similarly, I’d purchase Microsoft Office (perpetual license), over Microsoft 365 for my personal or business use, if I had concerns about future cash flow.

Providing products as a service requires confidence from suppliers as well. If I anticipate high inflation I wouldn’t sell any subscription that locks consumers into today’s prices. In a period of high inflation, I either want to make one-time sales today or To continue the car lease example:

A dealership anticipates a 10% inflation rate over the next year. In real terms, that means that a $200/month lease today is worth $180 monthly in one year*. As a result, the dealership will encourage its sales staff to push sales over leases, or to encourage customers to wait and purchase the vehicle at a later time (because the car will sell for more nominal dollars). The lease option will lock the dealership into lower revenue for an inflationary period.

If the average consumer does not believe that she will be able to afford a subscription in the future, demand for subscriptions will fall. When producers anticipate that their products will be worth more in the future, they will not sell contracts at today’s prices. However, when both producers and consumers have confidence in the economy and their future income, the as a service model makes a lot of sense for both parties.

The “as a Service” model can cut costs and reduce time from purchasing to use for consumers. Reducing time to value is most applicable in a business-to-business context where new software deployments can take months, but holds true in the business-to-consumer landscape as well. Learning to cook and stocking a kitchen takes time and expense, consumers are increasingly shifting to Food-as-a-Service providers such as HelloFresh to manage the recipe creation and ingredient sourcing. HelloFresh allows consumers to have a “homecooked” meal much faster, and with less hassle, than the traditional grocery store process would have required. In the IT space, the as a service model reduces the physical overhead and resources that a consumer requires to support the product–the producer covers those costs with the subscription fee. Producers benefit from guaranteeing future recurring revenue and can reduce overhead through an economy of scale (by supporting all consumers). The “as a Service” model is so attractive to producers that Microsoft intentionally steers their consumers to the 365 subscriptions, rather than promote the purchase and subscription options.

The “as a Service model” is certainly booming. In 2018, Gartner predicted that “by 2020, all new entrants and 80% of haptoral vendors will offer subscription-based business models [in IT].” I could not find statistics to verify the accuracy of the claim, but it was directionally correct, at minimum. The growth rate of Microsoft 365 supports the claim.

Although the Consumer Confidence Index remains lower than historical average, the rise in XaaS agreements tells a contrary story. When confidence in both the economy and individual future purchasing power are high, XaaS arrangements are mutually beneficial. I anticipate that a reduction in the Xaas industry will be a leading indicator of falling economic confidence or a rise in inflation–both important economic indicators.

*I acknowledge the relationship between inflation and future payments isn’t as simple as stated. Financing, Net Present Value, and disparate effects of inflation create a more nuanced interaction of monthly lease payment and real value.

Socrates criticized writing as a lesser form of communication. A tool of the forgetful to use in record keeping and trade:

[Writers] will cease to exercise memory because they rely on that which is written, calling things to remembrance no longer from within themselves, but by means of external marks.

Our inventions are wont to be pretty toys, which distract our attention from serious things. They are but improved means to an unimproved end,… We are in great haste to construct a magnetic telegraph from Maine to Texas; but Maine and Texas, it may be, have nothing important to communicate.

The radio, telephone, and television also promised to fundamentally worsen interpersonal communication. The English language survived, mostly unscathed. Most of the high school English curriculum was written prior to 1960, and students do not struggle comprehend the English of American authors from the turn of the century.

However, the rise of the internet, specifically Amazon shopping and Google, may fundamentally change English grammar.

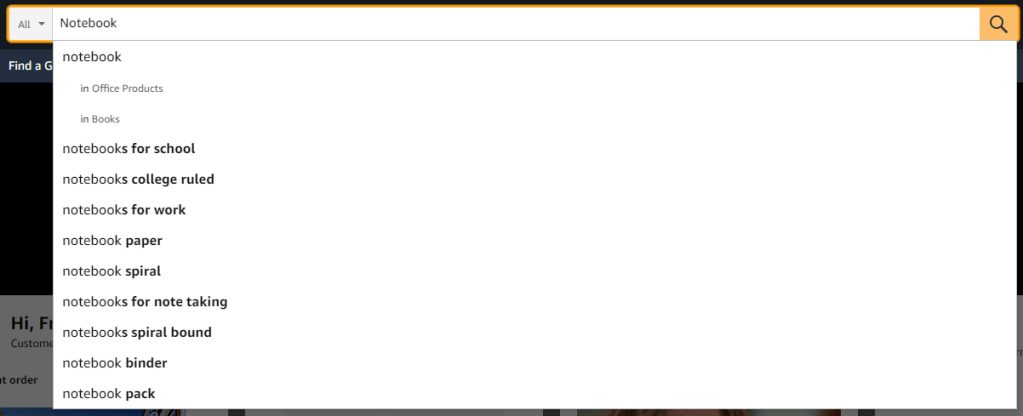

Without requiring formal study, native English speakers understand how to order words in a sentence. When describing an object, the descriptors generally lead the object of description. I have a red notebook. I use a large, yellow, fine-tipped, mechanical pencil. The general form of adjective placement for the English language is that adjectives precede the word they describe in the following order: Opinion; size; physical condition; shape; age; color; origin; material; purpose.

Not all languages follow this order. If I were to translate both sentences to French, they would translate literally as: I have a notebook red. I use a large mechanical pencil (mechanical pencil is a single word, so order of those words are irrelevant) yellow with a fine tip.

Many aspects of computing follow the romance structure of object then adjective. When storing or retrieving data, programs basically write a sentence, in the form of a script, that requests information from another part of the application or database. The “computing sentence” is most efficient and clearest when adjectives follow the object they describe. Although this phrasing might seem complex, let me introduce a familiar scenario.

When shopping for a red notebook on Amazon, I can either search for “Red Notebook” or “Notebook Red.” Both will take me to a shopping page full of red notebooks. In the search process; however Amazon takes a different route to find those notebooks.

When I look for a red notebook, Amazon starts by looking for red items.When the search starts with Notebook, Amazon will gather all notebooks as a starting point.

In this small search, the order doesn’t matter too much. Amazon has a powerful search engine and will react quickly to each new word. However, the path to the right notebook is more efficient when starting with notebook as my search term. When I type notebook first, Amazon recommends related searches and will limit suggestions to items related to notebooks. When I start with the word red, Amazon has to guess the next word based on the universe of items that could be red.

This image is obviously not to scale; however, if I were given the option to search either bubble for red notebooks, I’d want to start with all notebooks.

Computers are most efficient when objects are followed by descriptors. English speakers may find it more efficient to follow objects with descriptors in their internet search as well.

To revisit the red notebook example: When I search for a red notebook on Amazon, I’m given over 2000 results. Some are large, some are lined, some are bright, some belong with red fish, some with blue fish, some with one fish, some with two fish. To narrow my search, I add subsequent descriptors to my search. When I start with “red notebook,” I’ll likely end up with “red notebook hardcover lined 9×13” before finding few enough options to manually review. “Red notebook hardcover lined 9×13” does not follow any English grammar rules, and its uncomfortable to type. Amazon recommends additional words after my search, I end up with the unwieldy search by continuing to click the best fitting recommendations after each subsequent search. When I start with red notebook, Amazon recommends hardcover or paperback. I click hardcover. Still too many responses, I add a space to my search. Amazon recommends sizes. I click on the size. Too many responses. Etc.

Google works this way as well. When I search for something online and find too many results, I add additional criteria. That exercise of searching for an item and adding criteria with each subsequent search, is ultimately the same structure that Romance languages use in normal speech.

The advent of new technologies has certainly changed the English language. We have words to describe moving pictures, the internet, computer programming, and yellow fine-tipped mechanical pencils. However, these changes have been marginal. The internet, TV, and radio each added or standardized or added thousands of words, but the basic structure remained in tact. To call back to the beginning of the post, English teachers love to force Victorian literature on their students.

If the internet causes a single foundational, lasting change on the language, I think it will be a gradual shift in adjective order. Adjectives after the objects they describe are more efficient for the computer, more intuitive for online search, and are the norm for many other languages speakers that frequently use new technology. If English speakers continue to use online search for the next fifty years, and more people use voice recognition search, would it be crazy to think that the adjective order of the language will shift?

If Men were angels, no government would be necessary. If angels were to govern men, neither external nor internal controls on government would be necessary. In framing a government which is to be administered by men over men, the great difficulty lies in this: you must first enable the government to control the governed; and the next place, oblige it to control itself.

James Madison: Federalist No. 51

On Tuesday, January 6, the nation’s Capitol was overrun by a few thousand pro-Trump extremists. Their actions were treasonous, and it would be a disservice to our Democracy to call the events in the Capitol anything less than an insurrection.

In the address, Trump fell short of directly inciting violence, but encouraged those in attendance to “fight like hell” and to “stop the steal” of the 2020 election

After the address, the protestors started a planned march to the Capitol building to protest the certification of the election that will result in Joe Biden elected president of the United States

The cornerstone of American democracy has been the peaceful transition of power from president to president. As Ronald Reagan observed in 1981:

“To a few of us here today this is a solemn and most momentous occasion, and yet in the history of our nation it is a commonplace occurrence. The orderly transfer of authority as called for in the Constitution routinely takes place, as it has for almost two centuries, and few of us stop to think how unique we really are. In the eyes of many in the world, this every-four-year ceremony we accept as normal is nothing less than a miracle.”

Reagan would not be pleased with the state of affairs. Throughout the last year, president Trump refused to commit to a peaceful transfer of power to president-elect Biden:

The Trump presidency tested the mettle of the United States. This post started with a passage from the Federalist Papers about the principal struggle in establishing government. The structure and institution of government proved that the Constitution of the United States continues to be sufficient to limit the power of man throughout the Trump presidency.

Congress has not been as successful as the Court in limiting presidential overreach. However, Congress too was able to redress illegal action. Congress impeached president Trump in 2019, after the president attempted to barter military aid in exchange for Ukrainian investigations into Joe and Hunter Biden.

The framers aimed to put into place an executive with enough checks-and-balances, and sufficiently limited power, to ensure that the president of the United States would never become a king. The structures of government proved to be a resilient enough bulwark against tyranny to ensure democracy.

The will of the people may not be so resilient. Trump encouraged millions to distrust the results of a national election, he encouraged the 74 million Americans that voted for him to reject Biden as president-elect. Distrust of both the government and the press are at historic lows. Conducting democracy in an environment where citizens trust neither the government nor the press is a futile exercise.

The insurrection of January 6 highlighted the lack of will in government and citizenry to moderate extreme action. Allowing entry to the capitol was a choice. If a similar-sized crowd attempts to disrupt the inauguration of president Biden, they will not find the same success. Pentagon officials sent memos on January 4 and January 5 banning DC guardsmen from receiving ammo and riot gear, engaging with protesters (except for self-defense), sharing equipment with local police, or using surveillance or air assets without explicit approval from Trump’s acting Defense Secretary, Christopher Miller.

Is it wrong to compare these actions with the Black Lives Matter protests of the last couple of years?

It is not fair to compare the actions of extremists with the actions of peaceful protestors. And those that compare the entirety of the BLM movement with the actions of rioters on January 6, are making an unfair comparison. However, those that compare the state of the East Precinct in Seattle to the entirety of Trump’s supporters are no better. The ability to protest peacefully must be protected in a democracy for all positions (within reason).

The language for reporting protests must be standardized. Not everyone that attended Trump’s address on the morning of the 6th is a rioter. Most didn’t take part in an insurrection, they protested peacefully. The vast majority of those who attend a Black Lives Matter rally are not rioters. They protest peacefully.

The storming and abandonment CHOP in Seattle and the Capitol in Washington DC are examples of insurrection and should be reported as such. Similarly riots that destroy property, result in violence, or encourage lawless action, should be reported as such.

In even the extreme cases of insurrection, protestors exist. Attending a rally should not be reported as proto-criminal activity.

Comparing any two political movements is appropriate. It isn’t unfair or morally wrong to compare a pro-Trump movement with the Black Lives Matter movement. However, it is unfair to turn one example into a strawman to bolster another movement. In valuing democracy we must allow space for all opinions, especially unsavory ones, unless they incite imminent lawless action.

Putting it all together

We do not yet know how much the actions of a few thousand people on January 6 threatened the United States. During the insurrection, rioters gained access to strategic IT and physical resources that could easily be used in future threats against the US by foreign or domestic actors. The political will of the United States to respond to lawless action is weak. Trust in government institutions and the press is low.

Ironically, the institutions of government themselves have proven resilient to both the president and the number of citizens that wish to halt democratic process. At present, trust in institutions, especially the Court, should be much higher. The levees held.