I am the third of my name. The concept of heritage and genealogy were important aspects of my childhood. My last name is derived from the word armor-maker in French. The spelling and pronunciation changed with each new location and set of cultural influences my forefathers faced. We tell many stories within my family about our history and for the first time have the ability to add to, or in some cases disprove, the stories that shape my family’s self-conception.

Genetic testing solutions allow consumers to learn more about themselves and identify unknown relatives. The vendors that provide these tests, such as 23&Me or Ancestry promise to provide recipients with information about their health predisposition, their family tree, their physical traits, and their ancestry data. These promises present a compelling sales pitch to a person so enveloped by the stories passed down from generation to generation.

But I will not participate in genetic testing. At least not now. While learning about my past is important to me, it is the future that will prevent me from participating in any of the genetic testing services.

My genetic information is not just my own. If I am fortunate enough to have any children, they will inherit 50% of my DNA. My DNA belongs to them as well, and they cannot consent to having their genetic data shared with a 3rd party service. If there are consequences to my decision to receive genetic testing services, they would be powerless to combat them and likely just as vulnerable to those consequences as I am.

The United States has long realized the value of protecting an individuals personally-identifying health information. This information, covered as protected health information (PHI) is regulated under federal law (HIPAA) to prevent healthcare organizations from misusing or inappropriately distributing health data. Secure health information is critically important to a person’s safety, psychological and physical.

Let us consider a world without these protections. Imagine an elderly man who is suffering from a disease that may prove fatal previously had his health records distributed. Big Pharma buys those records and targets him with personalize adds that push unproven medication at high cost. Does that man have the presence of mind to consider those treatments rationally? Or does this predatory advertisement scheme, made possible by the release of health data, place this person facing his death in a psychological space that will result in overspending and potentially accepting treatment that lowers his quality of life. Consider a young gay consultant that travels internationally for work. Professionally, she keeps her sexuality private. Due to her medical records being sold, her clients based in a conservative country find out her sexual orientation and fire her.

These DNA test companies are not covered under HIPAA. The United States does not have a legal structure to suitably regulate what these companies do with their data. When these companies promise to provide reports on the recipients genetic indicators, physical traits, and medical predispositions, they are promising they have data that make the above scenarios possible.

The described scenarios are not only conspiracy fodder. DNA is not sufficiently protected and some of the privacy concerns have been proven valid. One of the DNA testing companies had a DNA breech in 2019 that revealed genetic and demographic data for 3,000 individuals. Law enforcement officers can require arrestees to take a DNA test without a warrant. In April 2018, US law enforcement legally used an online DNA match to catch a suspect, judges compelled the testing provider to open their database to a police search.

If US law enforcement’s use of DNA or a small leak are not sufficiently compelling, 60 Minutes ran an interview with Bill Evanina, the former director of the National Counterintelligence and Security Center, about China’s desire to collect American DNA data. I’ve added an excerpt below:

Current estimates are that 80% of American adults have had all of their personally identifiable information stolen by the Communist Party of China. The concern is that the Chinese regime is taking all that information about us – what we eat, how we live, when we exercise and sleep – and then combining it with our DNA data…

…Part of the social control includes the forced collection of DNA. Under the guise of free physicals for Uyghurs, Richardson says China is actually collecting DNAand other biometric data that’s then used specifically to identify people, target other family members and refine facial recognition software. And those, national security officials say, are just the uses we know about.

Currently, both Ancestory.com and 23andMe (the two biggest vendors in this space) claim strong privacy policies, and even allow users to delete some of their data (at the expense of future updates) that are designed to give their customers confidence that their data will be used responsibly and held securely.

That may be true.

But without a regulatory system that enforces genetic privacy, ensures total transparency on the transfer of genetic and demographic data and levies harsh punishment on data breeches, the risk of misuse is too high for me.

A final consideration. In 2018, U.K pharmacy giant GlaxoSmithKline invested $300 million in 23andMe, which included some exclusive access to 23andMe’s database. In December 2020, Blackstone Group, a global investment firm, bought Ancestry.com for $4.7 billion. In both cases users who purchased genetic tests prior to the investment/purchase now have their data managed or available to a corporation they may not trust as much as the company they purchased the test from. And given the sums invested, would it be rational to expect that these investors plan to maintain this store of priceless data without capitalizing on it?

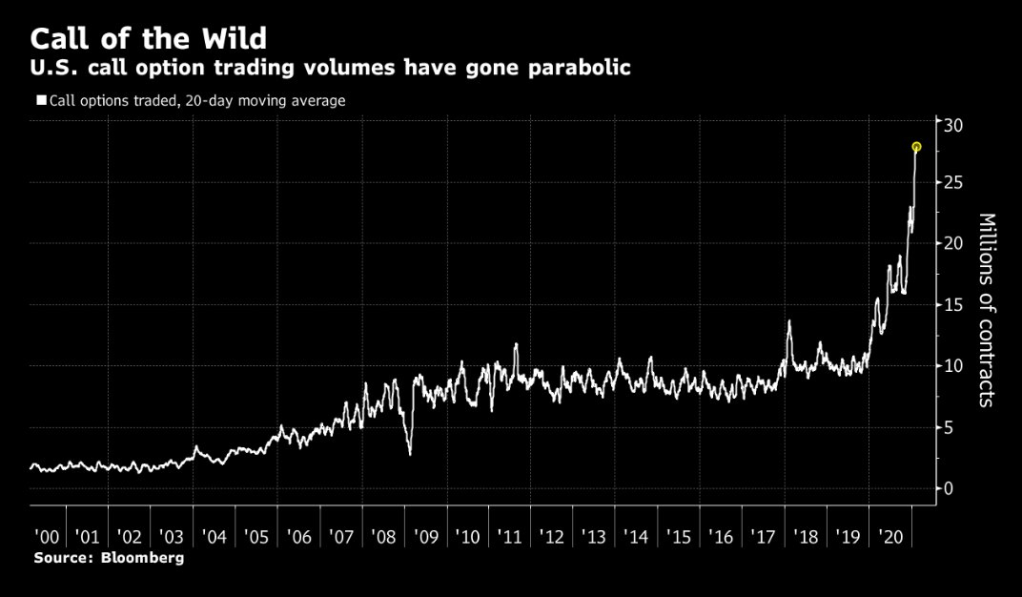

For a few days at the end of January 2021, GameStop, a brick-and-mortar video games retailer commanded every news headline. The company’s stock price, valued at $2.57 a share in April 2020, rocketed to a high of $483 a share on January 28, 2021. The company, formally valued around $300 million in market cap, was briefly worth $25 billion. There were no changes in the business that accounted for the change in price.

As of February 12, GameStop is trading at $52.40 a share. More than the paltry $3, but nowhere near its high. The GameStop rollercoaster is over.

Or is it? Although the stock price is beginning to level out, the controversy around GameStop is not yet over. After the stock price jump, and subsequent fall, market insiders and retail investors have started asking for additional regulation to protect their interests. The regulatory response battle will be a long one.

Hedge funds shorted the stock and there was opportunity to profit from a “squeeze.”

The second reason requires a little bit of explanation. John Cochrane describes the short selling process clearly in his blog:

Here’s how it works. A has GameStop shares. B, the short seller, borrows those shares from A, and sells them to C. Now both A and C can have long positions in the stock. We have doubled the supply of shares. Alas, this mechanism is imperfect. It only lasts a day. B must be ready to buy back the shares the next day and return them to A.

The shorts have two options, if the price does not fall:

Close the position– Pay the market value + interest for the stock to buy the underlying shares. Because B has to buy the stock at market value (that did not fall), B owns the shares and the price of the stock increases due to the increased demand.

Roll the position –B does not need to give the stock back on day 2, instead paying more interest each day to continue borrowing the shares from A.

The short selling of GameStop was so prolific that the shorts (B) borrowed more shares than have been issued. The WallStreetBets Reddit and YouTube communities jumped on the opportunity to buy shares, in the expectation that the shares would have to be bought at higher prices by the short selling entities. These communities have become increasingly large over the last few years, corresponding with the rise of fee-free brokers. Fee-free brokers with applications, such as Robinhood, allow individuals with any sum of money (the average account is less than $5,000 and owned by a 31-year-old) to participate in the stock market. Robinhood has over 13 million users; at the GameStop trading peak, analysts predict that nearly 50% of Robinhood users bought GameStop.

The squeeze started on January 12. On January 12, the stock closed at $19.95 per share. January 13? $31.40. January 25, $76.79. January 26:

January 27 closed at $347.51 per share. By February 2, the stock closed under $100 a share and the principle short sellers had closed their positions.

How did institutions respond?

During the period between January 26 and February 2, the stock was halted or paused a number of times by brokers and the New York Stock Exchange.

Robinhood, and similar broker-apps, restricted trading of GameStop and other highly volatile securities during this time. Users were, at times unable to purchase more shares or options of GameStop. Other application users reported that Robinhood actively sold their shares or options of the company, at low prices. Retail investors, understandably complained and demanded action from Washington:

LMAO omg I love when ppl w differences come together. Beautiful day out here on Twitter pic.twitter.com/uQ9xBany2j

These brokers were quick to respond that they were forced to halt stocks and restrict ownership based on current regulation or clearinghouse requirements.

When a Robinhood user buys a stock it actually takes two days for the funds to be exchanged (SEC standard), in the interim, Robinhood must post the colleterial for its users’ purchases. Due to Dodd Frank regulation, clearinghouses must set collateral requirements based on concentration of ownership and volatility of a stock. These brokers are not able to use their clients money to post colleterial (the theory is that these restrictions will prevent brokers from irresponsibly losing investor money when they go bust). Depending on the broker, either the clearinghouse forced a halt trading on GameStop, or the broker no longer had the liquidity required to cover the collateral requirements for trading the stock. As an example, the largest clearing organization (DTCC) reported that the industry-wide collateral requirements jumped from $26 billion to 33.5 billion on January 28.

Large institutional traders did not have the same liquidity concerns and were not halted by their clearinghouse agreements from purchasing the stock, or its derivatives.

So who made money?

The GameStop short squeeze was billed as a David-and-Goliath story of Reddit users taking down hedge funds. That isn’t exactly what happened. Short sellers initially lost around $19 billion, but none shuttered. It’s true that Melvin Capital (the hedge fund with the largest short position) required a bailout of about $3 billion from other funds, but hedge funds as a whole were not defeated by the short squeeze. Who made all of the money from the stock increase?

Not retail, generally. GameStop saw a $20.4 billion gain in market cap. Nine investors, led by Fidelity and BlackRock, totaled a $16 billion return on the GameStop short squeeze. These 9 firms made 75% of the total gain.

The returns were mixed for retail investors. Some early retail investors saw significant gains from their GameStop investment, most bought over $100 per share and received only modest gains or, more frequently, losses. When Robinhood limited its users’ ability to purchase stock or sold shares purchased with unsettled funds, retail investors were prevented from capitalizing on potential money making opportunities.

Will it happen again?

I am not a financial advisor, nor do I give financial advice. I am speculating on the frequency of a similar short scenario; rather than on the performance of any individual stock.

For a short squeeze of this magnitude, institutional players must have interests on both sides. Michael Burry and other investors publicly announced long positions in the company. Short institutional firms announced their interests as well. These types of public battles don’t occur often. Firms that take anti-shorting actions tend to have very low returns, making them unlikely targets for long-term value investors. For all of the publicity Robinhood and WallStreetBets received in the GameStop narrative, they did not have the power to push the GameStop stock alone. As noted above, the firms that cashed in on the run were major hedge funds. Institutional money was required to generate the momentum in the stock price.

Second, the short interest in GameStop was greater than the number of shares in circulation. As of February 12 2021, there are no companies in the S&P 1500 with short interest over 100%. While short squeezes occur with short interest well under 100%, the magnitude will not reach GameStop levels.

Retail short squeezes might become more common though. Small retail investors will attempt to replicate the GameStop experience on other stocks. Chat rooms, Reddit, and YouTube are not diminishing in size. The WallStreetBets Subreddit (community blog) grew by 2.4 million subscribers during the GameStop short squeeze.

Robinhood continues to grow as well. The tool enables small retail investors to trade stocks, as well as more complex derivatives, without fee. The rise in this app enabled a major rise in speculative investment by individual retail investors (the common folk).

After the introduction of transaction-free brokers, such as Robinhood, the number of options traded skyrocketed.

Another GameStop is unlikely, but the increase of speculative investing by small retail accounts will fundamentally change the trading behavior of some stocks. About a year ago, WallStreetBets pushed the stock of Lumber Liquidators through community action. The Lumber Liquidators example is more representative of the market power of the WallStreeBets community. I anticipate more of those stories as the platform grows and barriers to trading are removed through applications such as Robinhood.

If it’s unlikely to happen often, why should I expect regulatory action?

Regulators are receiving pressure from institutions and retail investors to prevent similar situations from happening. On the institutional side, the demand for regulation includes a crackdown on these forums to prevent coordination on certain stock strategies. Institutions calling for greater regulation of social media coordination point to the behavior as a form of market manipulation. GameStop is not the only stock that had a semi-coordinate strategy. The WallStreetBets community tried, to a lesser extent, to exert the same pressure on AMC, Nokia, and BlackBerry.

Retail investors are arguing for regulation that would further democratize the stock market. The nature of these regulations would be to open the number of investment vehicles available for retail investors, to protect trading chat rooms (CNBC is allowed to exist, how is a Reddit forum discussing stocks fundamentally different), prevent clearinghouses from being able to raise collateral requirements in a manner that restricts retail trading.

Although the nature of the regulation that will be introduced is unclear, it’s reasonable to expect a regulatory response. Treasury Secretary Yellen scheduled meetings with the SEC, the Federal Reserve Board, the New York Fed and the Commodities Futures Trading Commission to discuss the recent events in the market. Given the Tweets above, members of Congress are interested in proposing regulation as well. The CEOs of Robinhood and Reddit will testify this month before a House Committee.

Our regulatory system does a lot in the name of “protection” to keep people of low means away from the kinds of investments that wealthy people can access. I think it is likely that the majority of the regulation that comes from the GameStop hearings will attempt to limit “risky” retail behavior, rather than open the market further. I anticipate at least some of the following regulations will be put into place:

Small-broker applications will be reclassified as gambling applications and regulated in the same manner as sportsbooks (state-level)

Small-broker applications will need to change their user interface to reduce gamification of stock trading

Create minimum equity requirements on trading accounts that are able to trade derivatives

Create a framework for the SEC to hold forums accountable for any coordination on stocks that occurs on the platform

Although the GameStop story received a lot of press, its impact on the stock market and financial institutions of the United States was marginal. Any of the likely regulations above would almost certainly do more harm than was created by the GameStop short squeeze.

*Addendum–The relationship between broker applications and organization that purchase order flow was not addressed at all in this write-up. The example commonly found in the news is a relationship between Citadel and Robinhood. I intentionally left it out because it is not unique to the GameStop scenario, nor does it related to the underlying activity; however, I see these relationships as an area fertile for proposed regulation.

Socrates criticized writing as a lesser form of communication. A tool of the forgetful to use in record keeping and trade:

[Writers] will cease to exercise memory because they rely on that which is written, calling things to remembrance no longer from within themselves, but by means of external marks.

Our inventions are wont to be pretty toys, which distract our attention from serious things. They are but improved means to an unimproved end,… We are in great haste to construct a magnetic telegraph from Maine to Texas; but Maine and Texas, it may be, have nothing important to communicate.

The radio, telephone, and television also promised to fundamentally worsen interpersonal communication. The English language survived, mostly unscathed. Most of the high school English curriculum was written prior to 1960, and students do not struggle comprehend the English of American authors from the turn of the century.

However, the rise of the internet, specifically Amazon shopping and Google, may fundamentally change English grammar.

Without requiring formal study, native English speakers understand how to order words in a sentence. When describing an object, the descriptors generally lead the object of description. I have a red notebook. I use a large, yellow, fine-tipped, mechanical pencil. The general form of adjective placement for the English language is that adjectives precede the word they describe in the following order: Opinion; size; physical condition; shape; age; color; origin; material; purpose.

Not all languages follow this order. If I were to translate both sentences to French, they would translate literally as: I have a notebook red. I use a large mechanical pencil (mechanical pencil is a single word, so order of those words are irrelevant) yellow with a fine tip.

Many aspects of computing follow the romance structure of object then adjective. When storing or retrieving data, programs basically write a sentence, in the form of a script, that requests information from another part of the application or database. The “computing sentence” is most efficient and clearest when adjectives follow the object they describe. Although this phrasing might seem complex, let me introduce a familiar scenario.

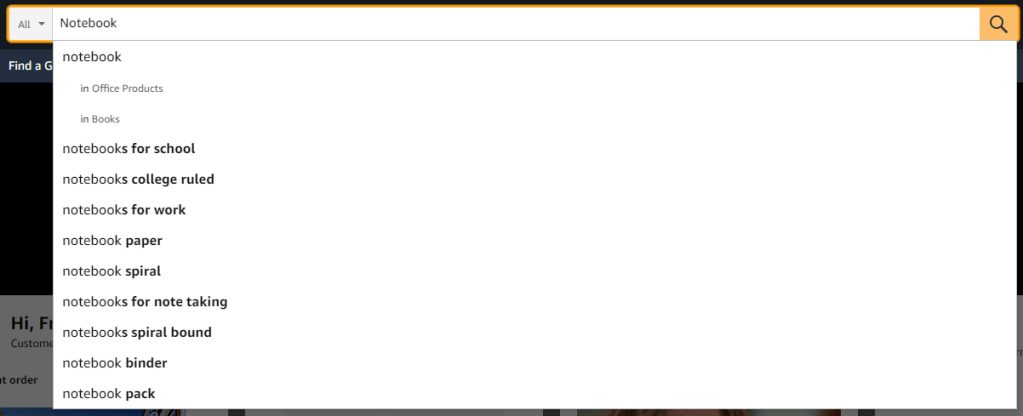

When shopping for a red notebook on Amazon, I can either search for “Red Notebook” or “Notebook Red.” Both will take me to a shopping page full of red notebooks. In the search process; however Amazon takes a different route to find those notebooks.

When I look for a red notebook, Amazon starts by looking for red items.When the search starts with Notebook, Amazon will gather all notebooks as a starting point.

In this small search, the order doesn’t matter too much. Amazon has a powerful search engine and will react quickly to each new word. However, the path to the right notebook is more efficient when starting with notebook as my search term. When I type notebook first, Amazon recommends related searches and will limit suggestions to items related to notebooks. When I start with the word red, Amazon has to guess the next word based on the universe of items that could be red.

This image is obviously not to scale; however, if I were given the option to search either bubble for red notebooks, I’d want to start with all notebooks.

Computers are most efficient when objects are followed by descriptors. English speakers may find it more efficient to follow objects with descriptors in their internet search as well.

To revisit the red notebook example: When I search for a red notebook on Amazon, I’m given over 2000 results. Some are large, some are lined, some are bright, some belong with red fish, some with blue fish, some with one fish, some with two fish. To narrow my search, I add subsequent descriptors to my search. When I start with “red notebook,” I’ll likely end up with “red notebook hardcover lined 9×13” before finding few enough options to manually review. “Red notebook hardcover lined 9×13” does not follow any English grammar rules, and its uncomfortable to type. Amazon recommends additional words after my search, I end up with the unwieldy search by continuing to click the best fitting recommendations after each subsequent search. When I start with red notebook, Amazon recommends hardcover or paperback. I click hardcover. Still too many responses, I add a space to my search. Amazon recommends sizes. I click on the size. Too many responses. Etc.

Google works this way as well. When I search for something online and find too many results, I add additional criteria. That exercise of searching for an item and adding criteria with each subsequent search, is ultimately the same structure that Romance languages use in normal speech.

The advent of new technologies has certainly changed the English language. We have words to describe moving pictures, the internet, computer programming, and yellow fine-tipped mechanical pencils. However, these changes have been marginal. The internet, TV, and radio each added or standardized or added thousands of words, but the basic structure remained in tact. To call back to the beginning of the post, English teachers love to force Victorian literature on their students.

If the internet causes a single foundational, lasting change on the language, I think it will be a gradual shift in adjective order. Adjectives after the objects they describe are more efficient for the computer, more intuitive for online search, and are the norm for many other languages speakers that frequently use new technology. If English speakers continue to use online search for the next fifty years, and more people use voice recognition search, would it be crazy to think that the adjective order of the language will shift?

The US government should take action that bolsters the US economy, even after the pandemic subsides, without writing blank checks to US corporations.

Why not continue direct investment in US corporations? The United States Congress already provided $25 billion in bailout funds to airlines alone this year, and House Democrats are pushing for more.

The United States Congress should sanction a World’s Fair for the summer of 2021 or 2022 depending on the anticipated longevity of the COVID pandemic.

Although a proposal for a World’s Fair initially sounds like an immature policy response, I think it would be strong policy, both symbolically and economically, for the American people.

The World’s Fair, as I imagine, would focus on showcasing four aspects of American society:

A Brighter Future–How technology and the nation’s youth will bring the United States into its brighter future.

American Made–How Farming and Manufacturing make America.

E Pluribus Unum–How immigration and cultural appreciation create the World’s Melting Pot.

American Life–Sports, Theatre, Design, and Art

Ideally the Fair would be held for a few months in a city that had experience with significant air, bus and rail travel, and could hold hundreds of thousands of daily travelers. To ensure maximum economic benefit and avoid political entanglements, I’d propose to hold the convention in a mid-sized city, in the middle of the country. Omaha, Minneapolis, Indianapolis, Detroit, St. Louis, and Oklahoma City are likely candidates. Once the Fair finished, its exabits would travel to the marquee cities of the United States.

As a part of the policy funding, Congress would appropriate funds for grants associated with each of the four showcases and to subsidize travel/hotel costs for every American (at a graduated rate based on income). Additionally Congress would pay for the costs of the expeditions and for the traveling show; the winning city would need to allocate funds for the grounds and any city-specific exhibits.

The World’s Fair will jumpstart the aviation, busing, and rail industries. Symbolically, the subsidized travel will indicate to the population that it is safe to travel. Financially, it will allow millions of Americans to leave their home state for the first time, and bring in foreign travelers. Even after the Fair terminates, I anticipate many Americans and foreign citizens will travel more frequently than they would have without the encouragement.

Congress will add stipulations to the grants for each showcase that encourage competition in certain, popular and positive, arenas. For instance, the grants associated with youth and tech should promote changes to the education landscape, reduce the barriers for at-risk youth, and inspire future corporates leaders. The Farming grants would reward a return to suitable, local farming and encourage new small farmers.

In order for the World’s Fair to make a noticeable impact on the US economy or society, Congress will need to spend a lot on it. The last US World’s Fair (1984) failed because it didn’t receive the investment it needed. The US needs the cultural equivalent of a Ferris Wheel or Eiffel Tower (both World’s Fair inventions) to inspire confidence.

To make the endeavor palatable for both parties, the Fair will need to be sold as a support to the airline industries and to small-and-large businesses first. I propose the following funding sturcture:

40% of grant money to A Brighter Future

40% of grant money to American Made

10% of grant money to E Pluribus Unum

10% of grant money to American Life

In this structure, Republicans can promote the fact that farmers and manufacturers received a 40% of the overall funding, more than the “Liberal causes.” Democrats can sell the Fair as a celebration of culture and Art, 20% of trillions is a lot of funding for diversity and arts events. Both sides and the public should support the funding of children’s programs and the airline industry.

Obviously a single Fair will not save the airlines or build confidence and togetherness in the US economy. That should not be the goal. The Fair would save the airlines and hopefully bolster travel for years to come. The Fair should introduce youth to new cultures and business ideas. Ideally the Fair would inspire future economic growth both through the grant recipients, and for visitors who walk away inspirited with their personal ideas on how to build their brighter future.

I aspire to be a moderately successful home cook. I have a few specialties and can cobble together a decent meal each night, but I clearly lack fundamental skills. My vegetables, rice and pasta look rustic at best. I dedicated the last weekend to improving all three. My goal was to create one batch of sticky rice and one plate of pasta that passed muster.

Did I do it? You should know that if a blog describes cooking, you’ll have to endure a novel before you are permitted to see the results.

I’ve read a number of cookbooks, watched Masterclasses, and YouTube videos to improve my technique. I found some to be incredibly helpful, Jacque Pepin’s knife skills are a perfect primer. Joshua Weissman offers a good series on how to cook at home. But after a weekend of practice, I learned as much about remote education as I did about cooking.

Students have a number of learning styles. Schools attempt to incorporate a multitude of learning styles in their instruction. The VARK model is a widely-used schema for cataloging learning preference that educators use to vary instruction. In the VARK model, there are four types of learners:

Visual–learners that best internalize and synthesize graphic information such as charts, diagrams, hierarchies.

Auditory–learners who succeed when they have the opportunity to listen and wrestle with concepts verbally.

Reading–These are good students (I kid). Reading/writing learners are best when given the opportunity to read and write about their subject matter.

Kinesthetic–For these students, learning is a physically active endeavor.

One can argue how well the public school system caters to each style, if the VARK model is an appropriate way to classify learning styles, or if learning styles exist. However, when I was attempting to better my cooking this weekend, it was clear that all of the learning styles referenced above were available to me. I listened to and watched videos (Visual/Auditory). I rolled dough, and rolled dough, and rolled some more (kinesthetic). I read recipes and descriptions (Visual). I’ve considered myself a visual-spatial learner, and had no problem learning through the combination of media available to me. On-line education upheld its promise.

Yet, something was missing in my culinary lessons. I wasn’t always improving batch-to-batch. Learning models frequently focus on how to plan lessons and engage students, but rarely outline the best way to curb bad outcomes or patterns. I intuitively know that I wouldn’t benefit as much from a golf lesson over Zoom, as I would in person. My swing needs physical correction and don’t have the spatial awareness necessary to correct from words alone. Similarly, I wouldn’t want to take a music lesson without an instructor present to help correct breathing, posture and adjust my movements in real-time.

I need a lot of lessons…

After a weekend, I made incremental improvement in my ability to roll pasta and cut noodles, make sushi rice, and consistently cut a range of vegetables. I would have improved faster if I received real-time physical corrections. Practice does not make perfect, practice makes permanent. Without immediate correction, I’ve further entrenched bad habits that I hope to learn enough to correct later. When learning to cook online, I learned my personal limit with the available media.

Not perfect, but an improvement over past attempts.

Many students will return to academia online this coming semester. Invariably, these students will miss out on a number of intangible benefits of traditional education. In addition, I worry that these students will miss out on having their bad outcomes or patterns corrected. Will it be as easy to foster challenging intellectual conversation over the Web? Will educators be able to help students course correct in any academic discipline in video lessons?

Remote pedagogy might be the best course of action for many this autumn. That is not a topic I want to engage. However, I predict that remote learning will benefit the students of math, technology, and the sciences. I won’t be surprised when it results in poor outcomes in philosophy, history, language and elective courses. I won’t be surprised when remote learning constraints are further used to reduce funding of the Arts. Remote learning is probably not suited for disciplines of nuance that require gentle but constant and immediate corrections from an engaged educator.